The U.S. jobs report showed a gain of 223K jobs, which wasn’t far off market expectations, albeit it was better than the previous report. Alas, the report also showed downward revisions for the previous jobs reports and little change in wages. Following this news, gold and silver slightly rose, while the USD experienced sell offs mostly against the Euro and Aussie dollar. This report is likely to keep resonating in the precious metals markets in the coming days. Looking forward, the main U.S. reports will revolve around consumer: retail sales and consumer sentiment. The JOTLS report will complete the labor market overview and PPI monthly update will come out. In Europe, the GDP for Q1 will be released and could move markets. Here is an outlook for May 11-15, 2015:

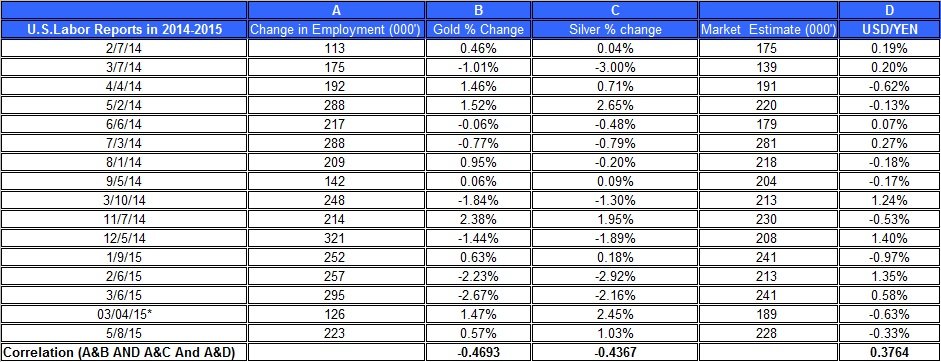

The NFP report was better than in the last report but didn’t come far off market expectations, and as you can see, the deviation from market estimates tend to move the gold and silver needle.

Source: Bloomberg, BLS website

The correlation among gold, silver and the deviations of NFP numbers from market expectations remain strong, as the table above presents. This could suggest that if the labor market doesn’t grow any faster in the coming months, this could give a second wind for a short term rally in precious metals prices.

For now, the news of the slower growth in the U.S. — the disappointing GDP for Q1 and now the NFP, which wasn’t weak but still wasn’t too impressive – has also driven down the market estimates about the next rate hike by the FOMC: The implied probabilities in the bonds market, shows that the odds of a rate hike in September have fallen to 23% and 54% in December. So even if the FOMC does pull the rate hike trigger, how much high could the cash rate be by the end of the year?! Will it be enough to drag down gold and silver to a new low?

Following the NF payroll report, this week the JOLTS report will be published, which is another report highly monitored by the FOMC, about the labor market. This report, however, tends to have a weaker impact on the bullion market.

Besides this monthly update, the main focus in the U.S. will be around the consumer with consumer sentiment and retail sales reports.

Last week another event that stirred up the markets was FOMC Chair Yellen’s comment about the high value of stocks. This comment isn’t likely to have a long term impact on the markets.

Finally, RBA, as expected, cut its cash rate again by 0.25 pp to 2%. This decision was expected and didn’t seem to have a strong impact on the forex and commodities markets.

By the end of last week, gold holdings in the GLD ETF fell again to 728.325 – a 1.81% drop compared to last week; The ETF’s gold holding are up by 2.25% for the year, up to date.

Takeaway

The recent devalue of the USD against leading currencies and the fall in the implied probabilities of a rate hike in the coming months pressured up gold and silver. This recovery, however, may not last long if the USD starts to come back. For now, the weakness of the USD could continue. Also, the NFP report is likely to echo in the coming days and keep gold and silver from pulling down. The ongoing fall in the gold and silver holdings in leading ETFs may suggest the demand for bullion is diminishing, which doesn’t vote well for precious metals outlook. Despite the lower odds of a rate hike in the coming months, LT bond yields rose in recent weeks, which could drive down gold and silver. These moving parts pull gold and silver in different direction, and all this suggests gold and silver may remain at their current levels. But I remain bearish on gold and silver for the long run.

For further reading see: